Construction Management is the highest circulation construction-based publication serving the UK built environment.

Opinion

Data | Construction fires back up, but pricing still vulnerable

Kris Hudson

As the reopening of construction gathers pace, Kris Hudson examines where construction output goes from here and why collaboration will be key to the sector's survival.

With the accelerating reopening of construction sites and

suppliers, June saw the fastest rise in construction activity for nearly two

years, according to the latest IHS Markit / CIPS UK Construction Purchasing

Managers' Index (PMI). After three

months of steep falls, new orders also stabilised, giving the indication that

the industry was finally reaching a stronger footing – albeit still shakier

than many had initially speculated.

We are certainly not out of the woods yet though. The Office

for Budget Responsibility (OBR) has revised its UK GDP forecast and now expects

a contraction of -12.4% in 2020. That represents the worst economic performance

in 300 years. If that rings true, the longer-term impact on the construction

industry, and in particular pricing, may be considerable.

This is not a paywall. Registration allows us to enhance your experience across Construction Management and ensure we deliver you quality editorial content.

Registering also means you can manage your own CPDs, comments, newsletter sign-ups and privacy settings.

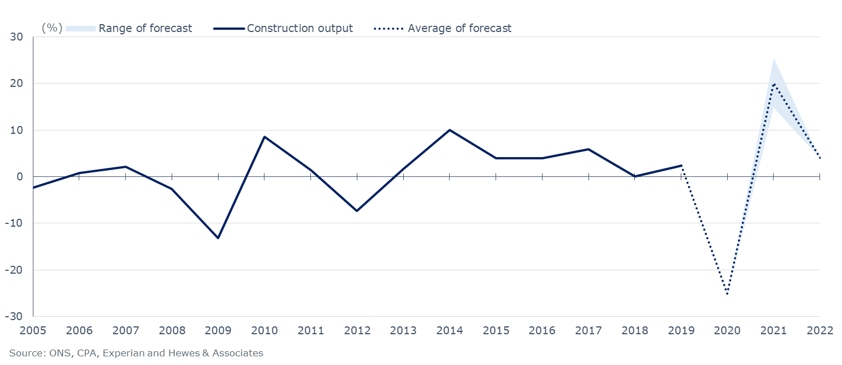

As a rule of thumb, construction output follows the

directional changes of GDP, but its movements are more amplified. The

Construction Products Association (CPA) finds that construction output can be

three times more volatile. Construction

is investment led and predominantly private sector driven – confidence is key

and any changes in sentiment can affect business decision-making.

Therefore, while the average forecast of construction output suggests a -25% fall this year, if we see a double-digit drop in GDP, a further reduction to output is not beyond the realms of possibility.

Construction output forecast for the UK

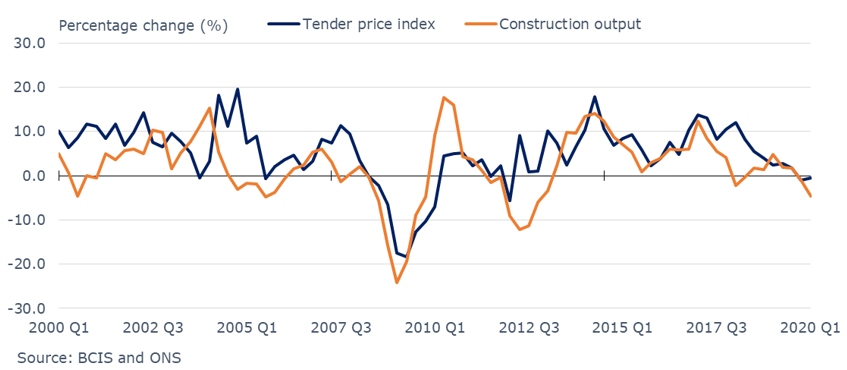

This is important because output also has a strong, positive

correlation with pricing. Our analysis shows that just over a third of the

variation in tender price inflation is driven by movements in construction

output.

Collaborate to survive

Decreased market activity typically leads to a more competitively priced market – and even deflation – as delivered output drops and investor confidence wanes. Contractors can become less selective over tendering opportunities and reduce prices, despite the risks.

Construction output index vs. tender price index, smoothed growth rate

The government’s infrastructure-led recovery may support

price stability to an extent but a simultaneous pickup in private sector demand

will be needed to avoid deflation. In the absence of this, deflationary pricing

and supplier insolvencies are likely to follow.

Against such a turbulent economic environment, we need to

preserve the capability that sits within our industry. Transactions looking to

exploit cost reduction opportunities will only hinder our supply chain in the

medium to long term, ultimately driving prices higher for all.

This recession will affect suppliers, consultants, contractors and sub-contractors alike – and it will take close collaboration to weather the storm.

Kris Hudson is associate director at Turner & Townsend

The January/February 2026 issue of Construction Management magazine is now available to read in digital format.

Powered Access

CM, in partnership with IPAF, has launched a new survey to explore the industry’s views and experiences with powered access machines on construction projects.

This is not a first step towards a paywall. We need readers to register with us to help sustain creation of quality editorial content on Construction Management. Registering also means you can manage your own CPDs, comments, newsletter sign-ups and privacy settings. Thank you.